This report was prepared in accordance with the requirements of Regulation 2/2016 of the Financial Supervisory Authority (ASF) regarding the application of corporate governance principles by entities authorized, regulated, and supervised by ASF, with further amendments and completions.

Considering the requirements of the above-mentioned regulations, Pool-ul de Asigurare Împotriva Dezastrelor Naturale periodically publishes and updates information subject to publication requirements.

Download the document in PDF format.

A. Organizational structure

The leadership and management of the company is made up of: the General Assembly, the Board of Directors, the Chief Executive Officer and the Deputy Chief Executive Officers.

Company shareholders on 31/12/2025*:

* Up to the publishing date of this Transparency report, the following changes were made to the ownership structure: Allianz-Țiriac Unit Asigurări S.A. became Allianz Țiriac Asigurări S.A. and the stake held by Euroins România Asigurare Reasigurare S.A. was acquired by Omniasig Vienna Insurance Group S.A.

The company shareholders hold together 19,341,819 shares in the company’s stock with a nominal value of 10 Lei, so currently the share capital of Pool-ul de Asigurare Împotriva Dezastrelor Naturale is 193,341,819 lei.

The five members of the Board of Directors are:

Executive Management:

In carrying out its activities, the management structure benefits from the support of nine boards and one advisory subcommittee. These operate according to organizational and operational regulations and make recommendations on various topics subject to the decision-making process and forward materials/reports to the Board of Directors on matters entrusted by it.

These boards are: the Risk management committee, the TIC risk management committee, the Audit committee, the Insurance Claims committee, the Petition analysis and resolution committee, the Investment committee, the Reinsurance committee, the Business continuity steering committee, the Remuneration committee and the Crisis committee for the disaster damage instrumentation plan. On 03/12/2025, setting up the PIM Committee was approved as a body within the governance system, responsible for overseeing the process of developing, validating, approving and using the Partial Internal Model.

Key roles: risk management, compliance, internal audit and actuarial functions.

The internal audit key role is outsourced to Deloitte Audit SRL. The internal manager responsible for outsourcing the role is the Head of the Internal Audit Department.

Critical roles: finance, legal, reinsurance, insurance claims, information technology, internal control and underwriting methodology, analysis and reporting. People holding key/critical roles are leaders of the mentioned organizational structures.

Structural organization:

B. The main features of the governance system

The governance system comprises organizational structures designed to support achieving strategic goals and the activity of the company. Pool-ul de Asigurare Împotriva Dezastrelor Naturale is properly and efficiently organized and all necessary operational procedures and controls are implemented. The governance system of Pool-ul de Asigurare Împotriva Dezastrelor Naturale is based on a proper and transparent responsibility distribution, which targets an effective decision-making process, preventing conflicts of interest and ensuring the efficient management of the company.

There are multiple systems within the company that are meant to achieve corporate governance, such as:

A series of policies and procedures were also adopted and implemented at company level, including policies/procedures to ensure smooth business operations; appropriateness policies; a remuneration policy; information security policies/procedures; outsourcing policy; a governance policy etc. These are subject to a regular review and approval process, taking into consideration the nature, scale and complexity of the activities at an individual and corporate level.

The Company’s objectives regarding the governance system are focused primarily on:

The organizational chart of the company and the Organizational and operational guidelines prove that the company has a structure suited for its nature, volume and complexity and the principle of proportionality is respected. The Organizational and operational guidelines also mention the roles and duties of the company's organizational structures.

In the reporting period, no changes were made to the organizational structure.

Further details on the corporate governance framework are available in the Solvency and Financial Condition Report (SFCR) Ch. B.

C. Financial position assessment conclusions

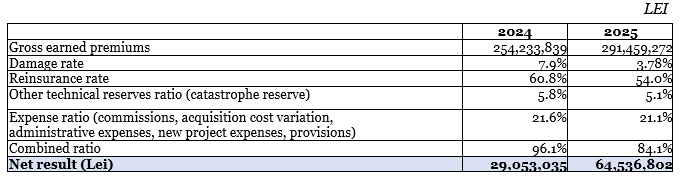

The main financial indicators of the company, according to the statutory accounting and financial reporting standards:

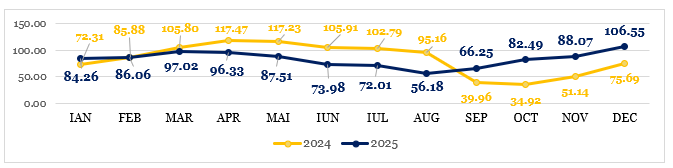

Evolution of the liquidity ratio, defined and determined in accordance with ASF’s methodology:

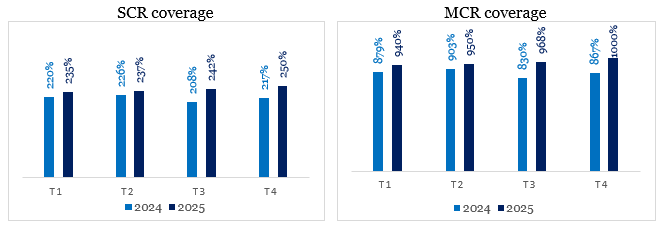

The main financial soundness indicators of the company, according to the Solvency II reporting regime, calculated using the standard formula:

In 2025, the solvency ratio (SCR) had a favorable trend, maintaining an upward trend from 217% in December 2024 to 250% in December 2025, driven by the lack of major events and the positive results achieved during this time. The MCR solvency ratio had a similar trend, raising from 867% in December 2024 to 1000% in December 2025.

Given the traits of the Company’s insurance portfolio, the Company’s risk profile deviates from certain assumptions underlying the Standard Formula.

On 03/04/2024, EIOPA made available for public consultation a proposal to amend the Catastrophe Risk included in the Standard Formula. The proposed amendment to the methodology, as included in the consultation materials, captures the significant impact of the “PAD franchise” on companies offering optional housing insurance, but does not address the exposure specific to the Company. The documentation clearly states that the recalibration does not cover the Company’s exposure. Under these circumstances, the Company has initiated a project to develop and validate a partial internal model. The project is currently underway and the pre-approval phase is expected to be completed in 2026.

The solvency capital requirement (SCR) on 31/12/2025 is 181,400,322 RON, and the solvency ratio is 250%.

To cover for risks taken on by the Company, on 31/12/2025, Pool-ul de Asigurare Împotriva Dezastrelor Naturale S.A. had an active reinsurance program with a capacity of 1.86 billion EURO, endorsed by a panel of 61 reinsurers.

D. Main features of the formal framework for the implementation of financial reporting principles and practices

Pool-ul de Asigurare Împotriva Dezastrelor Naturale draws up statutory financial statements in accordance with Regulation 41/2015 of the Financial Supervisory Authority for the approval of the Accounting regulations regarding annual individual and consolidated financial statements of entities conducting insurance and/or reinsurance activities.

Annual financial statements are audited by an independent auditor. The financial reporting package for fiscal year 2025 was audited by Forvis Mazars România S.R.L.

Reporting under Solvency II (SII)

In accordance with the financial reporting requirements of Law 237/2015 on the authorization and supervision of insurance and reinsurance activities and of Regulation 21/2016 regarding insurance and/or reinsurance activity reports, with further amendments and completions, Pool-ul de Asigurare Împotriva Dezastrelor Naturale draws up and reports:

In addition, in accordance with the provisions of the Solvency II Directive, the Commission Delegated Regulation and the internal policy, Pool-ul de Asigurare Împotriva Dezastrelor Naturale draws up an own risk and solvency prospective assessment report (the ORSA) annually or whenever important changes occur in its risk profile or risk appetite.

The “Reporting policy” was developed and applied to Pool-ul de Asigurare Împotriva Dezastrelor Naturale, whose purpose is to ensure the timely generation and forwarding of all mandatory reports, as well as their correctness and completeness.

The Audit committee is the forum that approves statutory and Solvency II reports before they are sent for approval to the Board of Directors and/or the General Assembly, as applicable.

E. Main features of the risk management system

The risk management system at the company level is implemented by planning, coordinating and controlling risk management activities.

Within this system, specific strategies are created, policies and procedures are developed for the timely identification, assessment, monitoring, management/reduction and reporting of risks in order to optimize them and to create a “risk-aware” organizational culture.

The purpose of the risk management system is to ensure the achievement of the company's goals regarding:

The specific risk management strategy is an integral part of the company’s general strategy, with the following fundamental objectives: meeting the SCR and MCR capital requirements and ensuring a high solvency ratio, achieving an optimum reinsurance programme and efficient management focused on operational efficiency and capitalization, all serving the single purpose of maintaining Pool-ul de Asigurare Împotriva Dezastrelor Naturale’s financial stability so that all its financial obligations to the Client are fulfilled.

Pool-ul de Asigurare Împotriva Dezastrelor Naturale annually creates a Risk plan which underlines objectives and measures for each significant risk, which is sent to the Board of Directors for debate and approval.

Pool-ul de Asigurare Împotriva Dezastrelor Naturale’s risk strategy is based on the following principles:

The Company’s main strategic goals are still related to the company’s 4 pillars of sustainable development, namely:

1. Governance: ensuring an operating framework fully consistent with legal requirements and the risk profile of the Company;

2. Financial sustainability: reflected by the company's solvency ratio and the appropriate size of the structure and level of reinsurance protection;

3. Operational sustainability: reflected in the ability to handle a much higher volume of operations than the usual average at any time in case of major events or expanding the portfolio;

4. Development: increasing the coverage of the housing stock via the mandatory home insurance (PAD).

Pool-ul de Asigurare Împotriva Dezastrelor Naturale S.A.’s activity is analyzed in terms of exposure to the following risks: underwriting risk, liquidity risk, credit risk, market risk, operational risk, reputational risk and strategic risk. Risks are handled both individually and cumulatively. The company calculates the capital requirement using the standard formula.

The results obtained give an overview of how risks are divided into various risk categories and establish capital and solvency requirements in accordance with Solvency II.

After the revision of the Delegated Regulation 2015/35, Pool-ul de Asigurare Împotriva Dezastrelor Naturale will be removed from applying the natural catastrophe risk sub-module of the standard calculation formula for the solvency capital requirement. Pool-ul de Asigurare Împotriva Dezastrelor Naturale will continue to use the standard formula methodology provided by EIOPA, except for this sub-module for which a development and approval project for an internal partial model is underway.

The company performs and develops quantitative and qualitative analyses for these risks in order to get a detailed image of the risks and especially to identify the necessary risk mitigation and control measures.

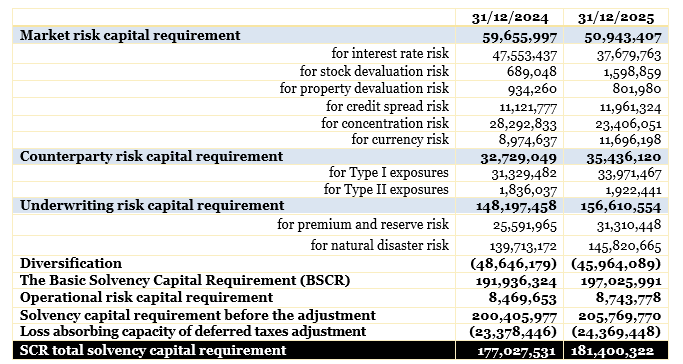

The quantitative results of the company’s most important risks are as follows:

More details on the risk management system are available in the Solvency and Financial Condition Report (SFCR) Chapter B (subchapter B.3) and Chapter C.

F. Conclusions of the assessment of the risk management system efficiency

Address:

Sos. Nicolae Titulescu no. 4-8, America House, East Wing, 3rd floor, Bucharest, postal code 011141Email:

office@padrom.roContact us at

0219930Work program:

Monday - Friday, from 09:00 to 17:00 (excluding public holidays)

RO

RO HU

HU